Australia enters 2026 with a housing market that remains resilient but is clearly shifting gears. After an exceptionally strong 2025—national dwelling values rose 8.6% across the year, driven by exceptionally strong markets in Darwin, Perth, Brisbane and Adelaide. Early indicators now point to moderation, continued uneven performance across cities, and heightened sensitivity to economic conditions, particularly cost of living pressures and market supply.

Where is the Market Right Now

Recent Cotality data (January 2026) shows the pace of capital-city price growth slowed towards the end of 2025 as affordability constraints bit and rate-cut momentum faded. Sydney and Melbourne recorded slight monthly declines in December 2025, while Brisbane, Adelaide, Perth and Darwin continued to grow, each sitting at record highs per Cotality’s Home Value Index.

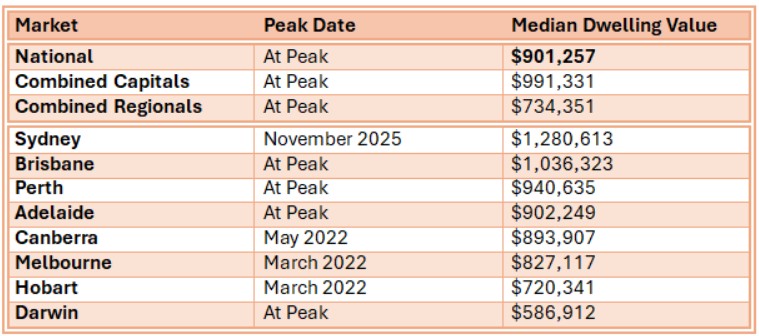

Current Dwelling Median Value as at 31st December 2025

Source: Cotality

Listings and Sales

Nationally, low listings remain the defining structural feature. New listings ended 2025 5% below the five-year average, although marginally above (1.1%) the same time in 2024, keeping markets tilted towards sellers. However, it is a slightly different story for total listings which were over 20% down on the 5 year average for the time of the year, indicating that there are buyers absorbing the supply.

Confirming that buyers are absorbing supply, total sale volumes were up 4.9% in the 12 months to December 2025, 3.2% across the combined capitals. Whilst median days on market increased slightly in the December quarter, the median days on market reduced from 27 days a year ago to 24 days currently.

Regional markets

Regional markets continue to outperform capital cities: annual growth for combined regionals (9.7%) exceeded combined capitals (8.2%), supported by relative affordability and lifestyle-driven migration. The strength of the regional markets, similar to the capital cities, is driven by supply, with total listings down 16.9% year on year and the median days on market reducing from 35 days to 32 days.

Rental Rates

Rental conditions remain extremely tight. Rents increased 5.2% nationally in 2025 and vacancy rates fell to 1.7%, from 2.1% a year ago. This is well below balanced-market levels and without significant changes in housing supply, we expect rental rates to continue to be strong into the future.

Housing Approvals

Monthly house and unit approvals have been consistently well under the 10 year average for the last 3-4 years. There was a spike in approvals for units / apartments late in 2025, however, with continued uncertainty in the economy, inflation and cost of living pressures at play, if developers are concerned about the outlook, necessary housing stock may not reach the market. Chronic supply deficits persist nationwide: Australia added 227,000 new households in the year to June 2025 (ABS) but produced only 175,000 new dwellings, intensifying upward pressure on both rents and prices.

Opportunities in 2026

Affordable Markets Outperforming

Lower-priced markets, particularly Perth, Adelaide, Brisbane and regional QLD & WA, are expected to continue leading growth as affordability ceilings in Sydney and Melbourne constrain buyers.

Units Regaining Momentum

Rising house prices and deteriorating affordability are shifting demand toward units, especially in Brisbane, Adelaide and Perth where unit rents and yields remain strong.

First-Home Buyer Activity Rebound

Government schemes (e.g., expanded 5% Deposit Scheme) are expected to lift first-home-buyer participation through early 2026, particularly in markets under $800,000. This can have an impact on affordability for first home buyers, with this increased demand putting upward pressure on prices in this segment, similar to what was evident in the second part of 2025.

Risks to Watch

Potential Rate Hikes

Any RBA increase would immediately hit borrowing power and could push Sydney and Melbourne into mild price declines, given their elevated debt loads.

Investor Credit Tightening

APRA’s new DTI restrictions may limit activity at the mid–upper end of investor markets and reduce demand for riskier lending segments.

Affordability Ceilings

Affordability is at historic lows: the median dwelling is 8+ times household income, requiring 11 years to save a deposit. Growth is likely to be strongest where affordability is still intact.

Slowing Migration & Softer Labour Market

Lower population growth and a gradual rise in unemployment will moderate demand and may limit price growth as 2026 progresses.

Bottom Line

Australia’s housing market begins 2026 in solid shape but facing clear headwinds. Expect a year of two halves: stronger activity in early 2026 driven by first-home-buyer incentives and tight supply, followed by a slowdown if the RBA moves to tighten interest rates. Growth will remain highly uneven—affordable markets and units are likely to outperform bigger capital cities and dwellings, while high-end markets in Sydney and Melbourne face more downside risk.

What we can be sure of is that the housing market will deliver its usual mix of surprises and staying informed will matter more than ever. If you’re planning to buy, sell, invest or simply want clarity in a fast-moving market, WBP’s team is here to provide independent advice and trusted valuations to help you make the right call.