Purchasing a house will be the most important financial decision most Australians make. To avoid the risks and make a wise investment, you need to be well informed.

Property experts often highlight the need to do your due diligence, but what does that mean? Tim Stafford, Head of Research at WBP Group, reveals the critical information property valuers collect for their due diligence and shows you the best place to find it.

How Bad is Housing Affordability?

Concerned about the economic impact Covid would have, the RBA moved to reduce the cash rate from 0.75% to 0.25% between February and March 2020. In November 2020, they cut it again to 0.1%. To provide additional support to the housing market, both state and federal governments increased the number and size of the housing grants they offered.

Experts predicted a significant fall in house prices due to Covid. Instead, the availability of cheap money and sizeable government grants saw home buyers rush to take advantage of this once in a lifetime opportunity. The most recent figures from the Australian Bureau of Statistics show new loan commitments at $33.278 billion, a 68% increase in a little over two years.

House prices have soared in line with the dramatic increase in new loan commitments. According to CoreLogic’s November 2021 market update, dwelling values in Australia are 21.6% higher over the last 12 months, the highest annual appreciation since June 1989.

But as a result of rising house prices, homebuyers have taken on ever-increasing amounts of debt just to get a foot into the market, so debt to income levels have soared. And because wage growth has been stagnant, housing affordability has become a significant issue.

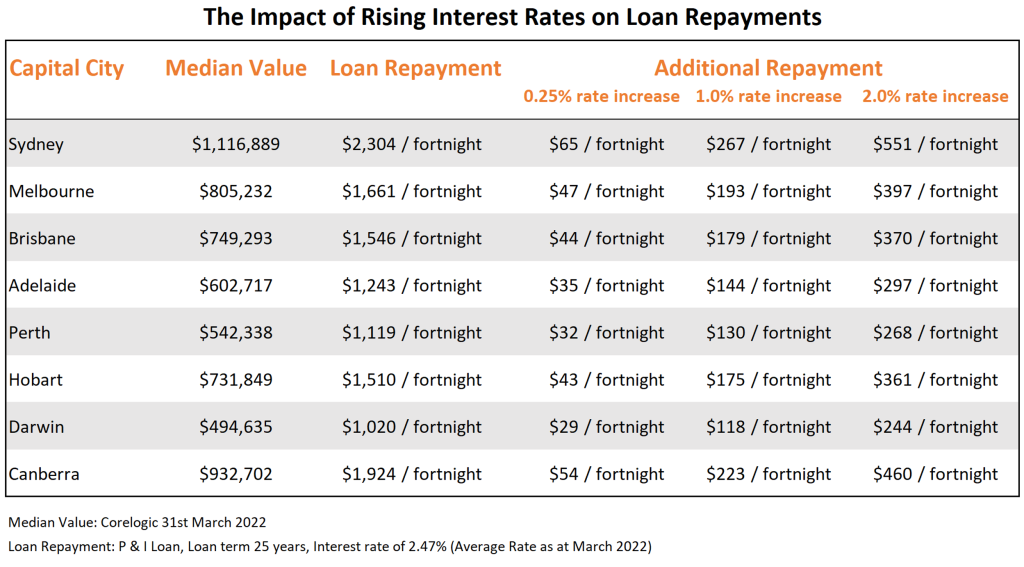

The recent rate rise means a home buyer looking to purchase a property at the median value in Sydney needs to find an additional $65/fortnight in their budget to afford that home. However, if rates were to increase by 2.0%, that same purchaser would need to find an additional $551/fortnight.

In Perth, where house prices are more affordable, purchasers need to find an additional $32/fortnight in their budget to cover the recent rate rise. If rates were to increase by 2.0%, they would need to find an additional $268/fortnight.

We’ve just been through a federal election where the cost of living played a substantial role. If the RBA continues increasing rates, housing affordability will only worsen. Do homebuyers have enough spare capacity in their budget to cover these increased loan repayments? The major banks think the answer to this question is no, given they’re forecasting house prices to cool in 2022 and fall in 2023.

In a November 2021 ABC News article, Commonwealth Bank head of Australian economics Gareth Aird pointed out, “the price that someone is willing and able to pay for a home is predominantly influenced by two things — income and borrowing rates.”

Mr Aird also noted that “as home prices move higher, affordability becomes stretched. That can be improved via a reduction in mortgage rates or higher income. But at some point the tailwind of lower mortgage rates on prices wanes unless there are further cuts in interest rates.”

Underlying Structural Issues

The rapid growth in house prices across Australia and the subsequent decline in affordability have resulted from strong demand and a limited supply of new housing.

No politician wants to see house prices drop on their watch, so state and federal governments have preferred to tackle the affordability issue by focusing on policies that make it easier to buy a house. Since the Global Financial Crisis in 2008, we’ve seen the First Home Owners Grant, stamp duty concessions, the First Home Loan Deposit Scheme and the First Home Super Saver Scheme.

While these policies have made it easier for homebuyers to enter the market, they are also responsible for stoking demand. Unfortunately, we’ve seen few policies that address the undersupply of housing, so house prices have continued to rise.

And now, the newly elected Labour government intends to introduce another policy to tackle housing affordability. They announced their shared equity scheme during the election campaign called Help to Buy, which will see the government enter into a shared ownership arrangement with home buyers.

In his July 2021 address to the Economic Society of Australia, RBA governor Dr Phillip Lowe expressed his view that government incentives were a root cause of rising house prices. But he also identified strong demand to live in fantastic global cities on the coast, a desire to live on large blocks and a chronic under-investment in transport as underlying structural issues that were also impacting the market.

Chairman of WBP Group, Greville Pabst, is aware that he is swimming against the tide with his prediction that house prices will rise in 2022 and 2023. In his Autumn Property Report, he noted that “what we are seeing now are vendors retreating from the market causing stock levels to shrink considerably, especially for detached houses.” He also wrote that “in my experience house prices do not fall when supply is tight. Throughout history, our property prices fall when we overbuild.”

We are likely to see two strongly opposed forces, housing affordability and demand, shaping the market for the foreseeable future. Will rising interest rates and cost of living pressures mean house prices fall? Or will the underlying structural issues in the market – government grants, limited supply and strong demand be enough to sustain further price growth?

Australians love to speculate on house prices, and it’s easy to get caught up in the short term movement of the market. If you’re contemplating buying a house in the next 12 months, I can understand why you would be questioning what will be the impact of rising interest rates.

While experts regularly disagree on what house prices will do in the next 12 months, there is a consensus that property should always be treated as a long term investment. So, the better question to ask is, where will house prices be in ten years. If I were a betting man, I would wager that prices will be higher than they are today.

If you would like to get more helpful valuation insights and property related news, follow WBP Group on LinkedIn.