Unless you’ve been living under a rock for the last four months, you would have seen that the RBA has moved aggressively to lift the official cash rate in an attempt to get inflation under control. Tim Stafford, Head of Research at WBP Group, speaks to some of our experts on the ground to see how the housing market has responded to this move.

What a difference 12 months can make. This time last year, the housing market was booming, with median values in nearly every capital city at record levels. It was also around this time last year when RBA governor Dr Phillip Lowe made his infamous statement that there would be no need to raise the official cash rate until 2024.

Since the RBA’s first-rate rise in May this year, market sentiment has taken a negative turn. In their July 2022 Monthly Housing Chart Pack, CoreLogic reported that national dwelling values fell by 0.2% in the three months to June. This decline was mainly due to Melbourne and Sydney, which experienced decreases in their dwelling values of more than 1.0%.

The CoreLogic report also showed a decline in sales volumes, with initial sales estimates over the June quarter 15.9% lower than the same quarter of the previous year. Another indicator of poor market sentiment is the combined capital city clearance rate, which averaged only 55.6% in the five weeks to July 3rd, down from 73.1% in the equivalent period of 2021.

Mohamad Zraika – Valuations Operations Manager, NSW

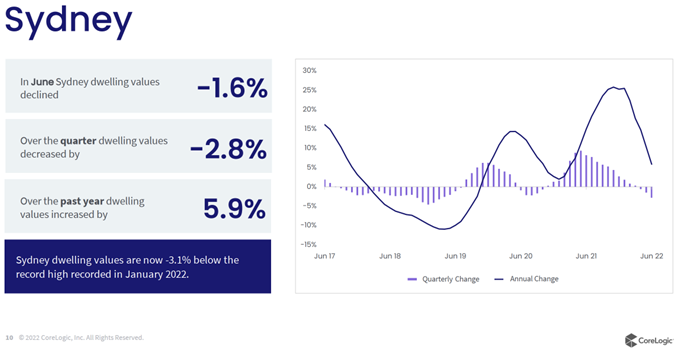

The Sydney market has felt the impact of the RBA’s decision to lift rates, with market sentiment the lowest it’s been in some time. Listings have declined, and most suburbs have experienced falling property values.

It appears that buyers now have the power and are steering away from less desirable properties, which have suffered the most significant drop in values. This switch in the balance of power has seen plenty of vendors opt for a price guide listing, and as a result, the auction clearance rate is down.

On a positive note, the more affordable regions in the west and south-west of Sydney have not been hit as hard, with the more affordable sub $850,000 market still performing strongly. The rental market across Sydney has also rebounded on the back of increased demand, and we have seen a significant increase in rental returns in recent weeks.

While the market has softened, agents are confident that vendors are simply waiting for the winter period to conclude before listing their home, so there is still an expectation of a busy spring.

Patrick Monaghan – Regional Director, Residential Valuations (VIC)

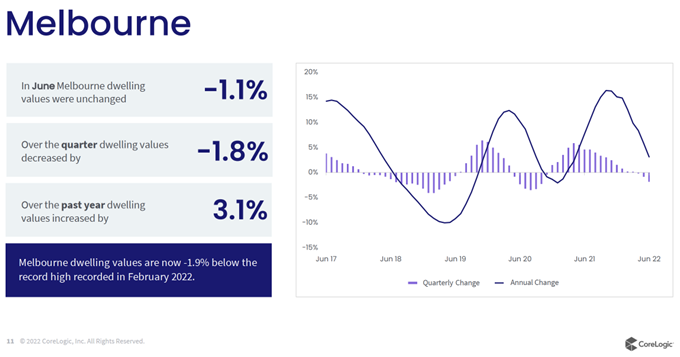

Four consecutive rate rises have created a two-speed housing market across parts of Melbourne, especially in the inner suburbs. Established family homes that have been well renovated and provide access to highly regarded schools remain in short supply. While they are not attracting the premium they did last year, they continue to perform well when sold at auction and do not appear to have experienced any decline in value

Properties in poorer locations or needing renovation have not fared as well, and the feedback we have received is that agents are finding these homes more challenging to sell. They’re often on the market for an extended period and regularly sell below their advertised range.

Given the difficulties new home buyers face obtaining finance and the uncertainty around how high mortgage rates will rise, current market conditions have seen many buyers apprehensive about bidding at auction. As a result, auction clearance rates have fallen. Buyers feel more confident when they can make their offer ‘subject to finance’.

Jonathan Millar – State Director (QLD)

The Queensland residential market has been solid over the past 12 months, and even in February and March this year, we saw some of the highest prices paid. However, of late, there has been a noticeable decline in sales volumes which we believe is primarily due to the increase in interest rates.

While there is a concern that house prices in the southeast may moderate given the rapid growth experienced there, the likely outcome seems to be a price correction rather than a significant downturn in the market.

There appears to be a consensus that the Queensland market will remain relatively busy moving forward, just not at the same level we saw at the start of this year.

Bart Quinn – State Director (SA)

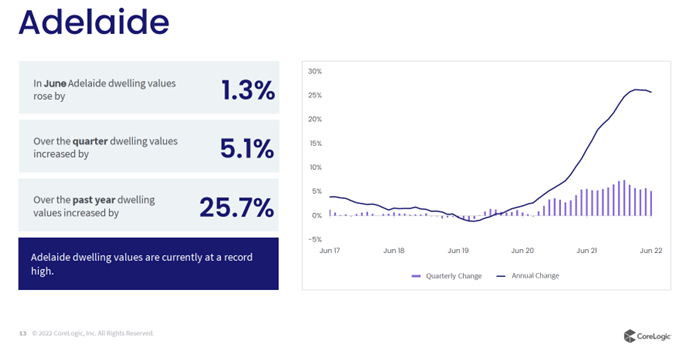

“The last 12 months in Adelaide have seen extremely strong competition in the housing market, and it was getting to the stage where values appeared to be well above justifiable levels. More recently, we’ve seen prices soften and a return to more ‘normal market’ conditions.

The feedback from agents across Adelaide has been that while they are seeing a reduction in the number of buyers for each property, they still have enough interest to achieve a sale price acceptable to the vendor.

In the areas where significant price growth was achieved over a short period, especially the middle northern to outer northern suburbs, we have seen some evidence that prices have retracted.

Donald Johnson – Senior Valuer (Perth)

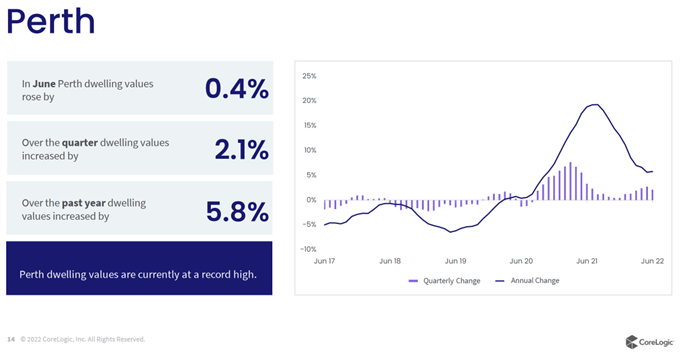

Since the RBA’s move to increase interest rates in May, we have noticed a shift in market sentiment throughout Perth. Homebuyers are acting more cautiously, given the uncertainty over how high rates may go, and they are taking longer to decide. Vendors are also more hesitant to list their property for sale in this market, so supply is constrained.

While the market has softened, it does not appear to have done so dramatically. And given Western Australia’s high positive net migration rate, the lack of new housing supply due to a lag in construction, and a comparatively cheaper property market compared to the eastern seaboard states, we expect to see more of a plateau in house prices than a substantial fall.

The good news for most homeowners is that despite falling prices, Corelogic’s July 2022 Monthly Housing Chart Pack reported values are up 11.2% over the last 12 months. And given Australia’s relatively strong economic position, low unemployment and undersupply of housing, it seems unlikely that house prices will fall off a cliff.

However, the news is not so good for anyone who bought a house in the last 12 months, because today, it’s likely to be worth less than what they paid for it.

If you bought in the last 12 months and budgeted for higher mortgage rates, you can wait patiently for the market to recover. But if you’re feeling the pinch of higher petrol prices, higher grocery prices, and now higher loan repayments, negative market sentiment means now is not the best time to be selling you’re home.

If you would like to get more helpful valuation insights and property related news, follow WBP Group on LinkedIn.