The 2023 property market proved to be one of surprise, but also of challenge. With rising interest rates, inflation and increasing cost of living impacting consumer confidence, the Australian property market’s resilience was again on show. It proved that the market is not predictable, and there are so many factors that impact performance and specific factors that will both drive or impact a particular segment.

When it comes to housing, performance across the capital cities varies substantially, driven largely by local factors such as supply, population growth, affordability and consumer confidence. We are seeing these factors play out right now and there are some interesting trends unfolding. Brisbane has now overtaken Melbourne and is the second most expensive capital city in Australia, with Adelaide and Perth quickly catching up to Melbourne.

Image Source: CoreLogic

Throughout this article, we explore what our valuations team are experiencing on the ground in our local markets.

New South Wales

Sydney

Mohamad Zraika, National Valuations Director

With rates being stable for the time being and speculation of a potential rate cut this year, prices of established dwellings are increasing across all the Sydney regions. Renovated dwellings are achieving premium value along with properties that are within short distances to metro localities. Unit valued remain stable, with little capital growth given the current supply levels in the denser localities. Low vacancy rates have seen investors re-enter the market with good rental yields being achieved in these areas.

Most properties are being sold within standard marketing periods and interest from developers is increasing for smaller two lot subdivisions in the west and southwest of Sydney. Prestige property more than $20 million, in the eastern and northern suburbs has attracted strong demand and continue to produce strong results.

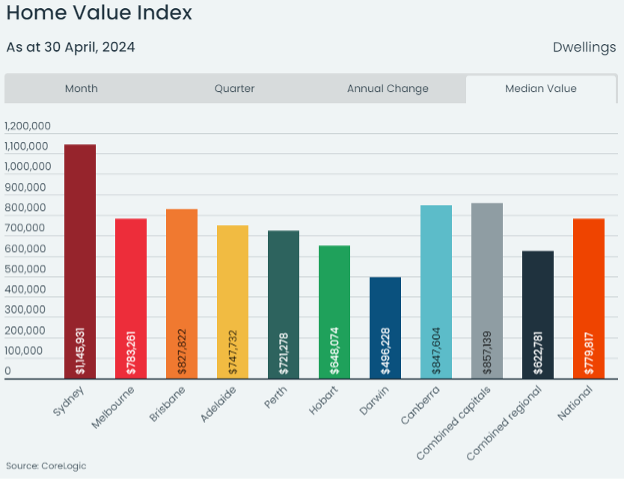

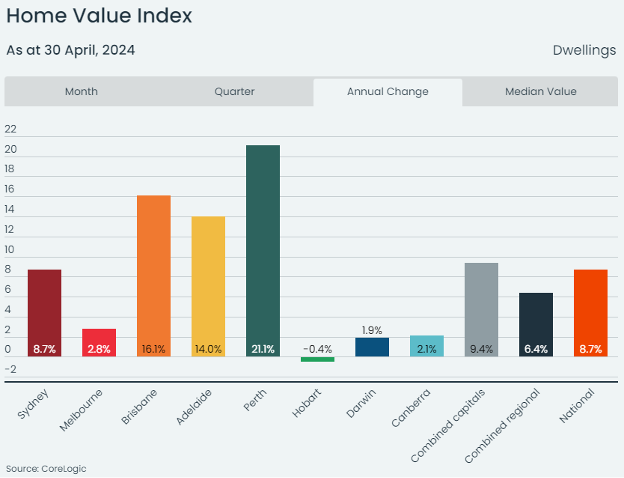

According to CoreLogic’s latest Home Value Index, Sydney’s median house price remains the highest in Australia at $1,145,931 and whilst not performing at the same rate as Brisbane, Perth and Adelaide, median values have risen 8.7% in the 12 months to April 30.

Newcastle, Hunter Valley and Central Coast

Cameron Michell, Managing Valuer

Andrew Walker, Property Valuer

The last quarter 2023, saw the local property market conditions soften with decreased buyer enquiry because of the higher interest rate environment. However, the Newcastle and Central Coast property market has bounced back with increased activity and some street and suburb records broken for the first quarter of 2024, offsetting any potential slowing in values which may have resulted from the uncertainties which were occurring towards the end of 2023.

Properties around Maitland and Hunter Valley appear to have remained stable for the first quarter of 2024. Vacant land values appear to have softened, likely based on affordability concerns, along with increased construction costs which have seen some buyers priced out of the market. Currently the area is seeing increasing levels of stock on the market and an increasing in selling periods. Whilst the increased stock has not yet impacted local values, there is the potential if stock levels continue to increase.

Local agents are indicating stronger attendance to open homes and increased buyer enquiry. The Newcastle, Hunter Valley and Central Coast markets are all continuing to benefit from non-local investors, looking to invest in more affordable, lower entry level regional cities and townships with higher affordability in comparison to the nearby Sydney market.

Illawarra & South East Coast

Simon Young, Director

Rachael Vilarinho, Director

The residential market started relatively bullish in the first quarter of 2024 with the prospect of lowering interest rates in the latter part of the year generating uncharacteristic demand from investors seeking to beat a potential rise in the market. With stronger than anticipated inflation rates persisting into the second quarter, we have seen prices stabilise.

Entry level market under $1m, has fared well due to affordability and is popular, albeit limited, with first home owner purchasers and investors looking to benefit from the strength of the rental market. Properties in the $1.25m-$2.00m price point are the most adversely affected properties in the region, due to most buyers in this price point being more economically sensitive to interest rates increases and the impact of the worsening cost of living crisis. Expectations in the marketplace are for stable market conditions to continue for the short term at least.

South East Queensland

Brisbane

Jonathan Millar, State Director (QLD)

The residential property market in South East Queensland continues to remain strong for dwellings, quality units and townhouses. Market drivers continue to be affordability, strong rental returns in comparison to other capital cities and solid interstate migration levels.

Brisbane dwelling values have risen approximately 3.1% in the last three months to end of April 2024 and 16.1% over the last 12 months. According to CoreLogic’s latest Home Value Index, Brisbane’s median house price has now taken over Melbourne and is the second highest in Australia at $827,822. This strong growth in the last 12 months has come along after a reduction in average values experienced during the second half of 2022 into early 2023. Since this point in time, Brisbane has experienced an upward trend in dwelling values for fourteen consecutive months.

With government infrastructure projects proposed and underway in Queensland over the next few years and in the lead up to the 2032 Brisbane Olympics, relatively low stock levels and solid continual demand, it is expected that properties prices will remain strong into the future. It will be interesting to see if affordability challenges place pressure on values now that Brisbane prices are the second highest in Australia.

Gold Coast

Like Brisbane, the Gold Coast is experiencing strong migration, a tight rental market and relatively strong sales activity. Low and high-rise apartments, especially in traditional investor locations such as Surfers Paradise and Broadbeach remain popular. Unit values are increasing, especially at the more affordable end (up 10% in last 6 months), due to generally low supply. The entry level for reasonable quality 1-bedroom units is close to $400,000 with rental returns of between $450-$575 per week if fully self-contained and furnished.

The prestige market is also strong, with a beach front property in in Jefferson Lane Palm Beach breaking the local record and selling for $10m.

Sunshine Coast

The Sunshine Coast continues to remain a popular location to invest/buy and re-locate. The investor market is driven by yields, which are reducing due to higher prices and rents not keeping pace. The unit market does not appear to be increasing at the same pace as the Gold Coast and inner Brisbane.

Good quality dwellings selling close to Noosa, Noosaville and Tewantin continue to show rises in value due to lack of stock and being well positioned close to water. SMQ research predicts a 4-6% growth in 2024 and a BIS Oxford report predicted 19% growth in the median Sunshine Coast house price over the next three years.

The prestige market is strong with one residence in Ross Crescent, Sunshine Beach, having excellent ocean views and sitting upon a large 3,520sqm parcel of land, selling for $28m in December 2023.

Victoria

Melbourne

Steve Kakavoules, National Director – Valuation Performance

Residential

After a lowered number of listings in 2023 offering limited stock to the market, 2024 commenced strong. However, since then, stock levels have tapered. Investor grade property continues to be a factor with increasing supply to the market due to higher borrowing costs and increased Land Tax, reducing investor returns and confidence. Although building costs appear to have settled, building approvals are at the lowest level in over 10 years, and there remains a lack of confidence in the sector, with many properties which require renovation, extension or capital investment, struggling in the market.

The Northern and Western growth corridors are now seeing supply increases with newly titled land ready for construction. Prices throughout south and eastern Melbourne remain steady, due to lower supply levels, however, pricing a property correctly is critical to a successful campaign and compromised property (main road location / properties requiring renovation), continue to struggle. Low vacancy rates are resulting in higher returns for CBD units. The Mornington Peninsula, which experienced unprecedented growth throughout COVID, has seen a large increase in supply on the market, impacting values.

Commercial

Joshua Ruzzier, State Director Commercial Valuations

The peak of the market for a majority of commercial Property, was in the last quarter of 2021 when the cash rate was 0.1%. The office market continues to be challenged in 2023 as businesses grappled with the post Covid working environment, with more work from home and hybrid working conditions, reducing the traditional office space requirements for many businesses. These structural changes to how businesses are operating looks like it is here to stay. Office vacancy rates remain high and incentives of between 20-40% are common in the market currently.

The continued surge in in online shopping has continued to drive the warehousing market with industrial property outperforming most sectors in recent years. However, a productive industrial construction sector has seen an increase in supply, predominantly across the eastern states, leading to higher trending vacancy rates and steadying market conditions towards the end of 2023. Industrial demand remains steady in 2024, albeit supply is catching up and we are seeing a slowdown of price growth and slightly weaker yields. There is strong industrial owner occupier and tenant demand particularly for <3,000sqm sites in the east and south east of Melbourne.

The retail market continues to show resilience and signs that conditions are returning, albeit slowly, to pre covid conditions. Vacancy rates throughout 2023 reduced, but remain above long-term averages, and although the cost of living has reduced consumer spending at an individual level, population growth has helped to fill the void.

Geelong & Southwest Victoria

James McGrath, Director (Geelong & Southwest Victoria)

The broader Geelong market is remaining relatively steady and is showing signs that the market has steadied, and the bottom may have already been reached. Established renovated family homes are still performing and attracting competition from multiple perspective purchasers however vacant allotments or dwellings which require significant work and upgrading, are generally being assessed in a cautious manner by the market overall.

The beachside and surf coast market remains slow. There has been a steady increase in supply on the market, with many ‘holiday home’ assets making up a large percentage of the stock and is an early sign that the increase in land tax in Victoria is starting to bite and further impact the cost of living for those with investment properties and holiday homes. With increasing supply and fewer buyers, its likely there will be downward pressure on values for holiday homes in the immediate future.

Regional Victoria Rural market

Brendan McKinnon, Director (Western Regions)

Dryland cropping land in the Wimmera/Mallee regions of Victoria has shown no signs of a reduction in levels of value over the past 12 months however the number of potential purchasers has steadied. The main reason for the continued demand is the price for grain to be at good levels especially for pulses such as lentils and canola.

In the same period grazing land south of Horsham has shown a dramatic reduction in prices due to decrease in prices for wool, lamb and beef, with reductions of between 25 to 40%.

Notable Sales:

An approx. 2,200-hectare parcel of land in the wheat growing area south-west of Mildura, was recently auctioned with a sale price of $2,000 per hectare. The area has very sandy soils and annual rainfall of about 220 to 250 mills, with this sale being well above previous sales which were in the vicinity $1,200 to $1,400 per hectare.

An approx. 750-hectare parcel of land between Horsham and Hamilton, recently sold for $5,060 per hectare. The land comprises blue gum regrowth that will need to be removed and pasture re-established. Approx cost estimates to do this are in the vicinity of $2,500 per hectare and it will take 12 to 18 months.

Adelaide

Bart Quinn, State Director (SA)

Residential

The Adelaide property market has experienced a sustained period of growth that has not yet shown signs of slowing. According to Corelogic the median house price increased by 1.3% in April, 3.3% over the past 3 months and 14% over the past 12 months. With Adelaide the median dwelling value currently sitting at around $747,732, which now exceeds the median price of Perth and now not far off Melbourne’s. Some industry experts are also predicting that the median price in Adelaide will exceed that of Melbourne, something that was unimaginable prior to the recent boom.

Over the past 12 months, and particularly the start of 2024, the outer northern suburbs have experienced the strongest growth, being underpinned by overseas migration. Prior to Adelaide’s Northern Connector opening in 2020, the outer northern suburbs of Adelaide experienced little growth and often longer marketing periods than many other parts of Adelaide. This is now a different story with agents reporting increased buyers through open inspections and low stock levels resulting in multiple offers, often in the first week of a campaign. As a result of the strong demand, many developments have been fast tracked to capitalise on market conditions.

Interstate investors have contributed to demand and growth, being attracted to the strong rental returns over the past 2-3 years. The prestige market has also experienced a sustained period of growth with an ever-increasing number of properties now transacting in excess of the $3-5 million range. Inner suburban units have also performed well, as prices have increased, units are now the only option for buyers with a limited budget seeking a cosmopolitan inner suburban lifestyle. Many inner suburban single level two-bedroom units have increased by around $200k over the past 2-3 years. Due to recent price growth and cost of living pressures, first home buyers are unfortunately finding it difficult to enter the market.

Commercial

Chris Wakeham, State Director (SA)

The commercial market in South Australia experienced a boom period across the last 2 to 2.5 years with high levels of buyer activity and demand and limited supply of stock, resulting in somewhat unprecedented capital growth within metropolitan Adelaide.

The industrial market has performed strongly throughout 2023 and in the early part of 2024, underpinned by a lack of supply of both established existing industrial property and industrial land which is suitable for new development. The sub 3,000 sq. m. industrial market appears to have the highest level of market activity, particularly from the owner occupiers.

The Torrens-to-Darlington (T2D) upgrading of South Road project has resulted in a notable volume of commercial properties positioned along the stretch of South Road to be upgraded (approx. 10.5 kilometres) requiring compulsory acquisition. As such, there is a number of tenants & businesses having to relocate – with a lack of supply of vacant properties available. There is clear evidence of active buyers in the market who require new premises (particularly owner occupiers), resulting in competitive campaigns and some strong results – particularly through the inner western and southern suburbs. In addition to this, the lack of available space has placed upward pressure on rental rates with local agents advising rental incentives are somewhat uncommon and typically not required at present.

Perth Metro

David Shorter, State Director (WA)

The Perth property market remains very strong and according to CoreLogic’s latest Home Value Index, Perth’s median house price is now $721,278 and has clearly been the strongest capital city over the last 12 months, with median values increasing 21.1%. Perth looks set to outperform the rest of the market this year with 6% growth over the last quarter and 2% last month and this is despite the median house price being at record high levels.

The market is largely driven by historically low supply, strong demand from owner occupiers and investors, with many investors, both local and interstate, attracted by strong returns.

Source: CoreLogic