After living through the ‘lost years’ of the pandemic, Gen Z (the demographic cohort born between 1997 and 2010) is anxious to get on with their lives. They aspire to fulfil the Great Australian Dream, but how will they ever afford to do so with skyrocketing house prices?

Adam Trenorden – Valuer WBP Group SA

As the Covid pandemic took hold in the first half of 2020, fear was in the air. There was an expectation of a prolonged downturn in the economy. Many of Australia’s leading economic forecasters predicted house prices would fall on the back of an extended period of high unemployment.

The Commonwealth Bank, Australia’s biggest home lender, warned house prices could tumble by as much as one-third in their worst-case scenario. But they weren’t the only ones predicting doom and gloom. All the major banks were forecasting at least a double-digit fall in property values.

Seeing an opportunity to enter the market at a discounted price, first home buyers led the charge. They were also keen to take advantage of record-low interest rates and generous state and federal grants. These grants have included the First Home Loan Deposit Scheme, First Home Super Saver Scheme, First Home Owners Grant, HomeBuilder grant and stamp duty concessions.

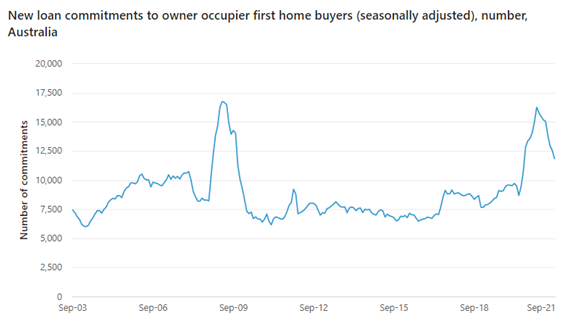

Figures from the Australian Bureau of Statistics (ABS) show a dramatic spike in the number of loan commitments to first home buyers starting in May 2020. Commitments peaked at just over 16,000 commitments in January this year. And while the latest ABS figures show commitments have fallen, they remain well above the long-term average.

While there was a slight dip in the market, primarily due to the uncertainty of Covid, house prices across Australia took off in the second half of 2020. Today, property values in every capital city, except Darwin and Perth, are at record highs. And according to CoreLogic’s November 2021 market update, dwelling values in Australia are 21.6% higher over the last 12 months, which is the highest annual appreciation since June 1989.

As house prices continue to climb, Gen Z is acutely aware of the challenge they face today trying to enter the housing market. Having just turned 22, Adam Trenorden has spent the last 12 months training as a cadet valuer at WBP Group’s South Australian office. In that time, he has had a front-row seat as dwelling values in Adelaide increased by 20.1%.

Even though house prices are at record highs, Adam is still committed to buying his first home, and he is not alone. A national survey of more than 1,600 Australians completed by Bankwest at the end of 2020 showed 71% of Gen Z were interested in owning their own home at some stage in the future.

Gen Z is optimistic about their prospects of entering the housing market, with just 3% of survey respondents believing that homeownership would never be achievable. Surprisingly, this figure is well below older generations, with 16% of millennials and 24% of Gen X resigned to the belief that homeownership is now unattainable.

Having finished his cadetship, Adam is one of the lucky ones who, during the pandemic, has found full-time employment as a residential property valuer at WBP Group. Because he feels secure in his job, he believes he’ll be in a position to enter the housing market in the next 2 – 3 years.

However, finding meaningful long-term employment is still a big issue for Adam’s generation, with 36% of Gen Z expressing negativity towards their job security.

Bankwest General Manager Home Buying Peter Bouhlas said: “We know the challenges of 2020 remain for many, and Gen Z, representing much of the young, casualised workforce of the country, often balancing study commitments, are greatly impacted by those challenges.”

Ongoing lockdowns and economic uncertainty have prompted an increase in household savings ratios, according to the ABS. So like 27% of Gen Z, Adam has begun the process of saving for a deposit. With full-time employment, he is in a position where he can contribute a sizeable portion of his salary towards this goal. It helps that, like many of his generation, he lives at home with his parents saving on rent.

Housing affordability remains a critical issue for first home buyers. Brendan Coates, economic policy program director at Grattan Institute, told Business Insider Australia the overarching story over the past two years has been a growing divide between haves and have-nots driven by the Australian property and rental markets.

First home buyers can pay a higher price if their parents are financially secure and willing to offer monetary assistance. And given the recent strength in the housing market, parents feel more confident tapping into the equity in their family home.

Parental assistance could include going guarantor on their child’s loan application which means their child will avoid paying lenders mortgage insurance if they haven’t saved a 20% deposit. It may also include an interest-free loan to purchase the house, or parents may simply offer their child a cash gift.

Research from Digital Financial Analytics showed that close to 60% of first home buyers sought assistance from the Bank of Mum and Dad (BOMAD) in the September 2021 quarter. Their research also shows that BOMAD has become Australia’s ninth-largest lender.

First home buyers who cannot rely on their parents for financial support find it more challenging to enter the market. Typically, the only affordable option is moving to one of the many new housing estates developers are building in the outer fringes of our capital cities. While you can find a decent-sized house with a backyard in your price range, the catch is, you’ll have poor access to public transport and schools as well as little or no amenities.

Adam has spent his life in and around the Adelaide Hills living in one of the more established suburbs developed post world war two, and this is where he would like to stay. He is not interested in moving to the outer fringe.

But to stay in the Adelaide Hills, he will need to compromise. Adam has accepted that when the time comes for him to buy, the type of house he will afford will be notably different from the type of house he could have purchased before the pandemic. Even so, Adam is committed to securing his Great Australian Dream.

If you would like to get more helpful valuation insights and property related news, follow WBP Group on LinkedIn.