Everyone wants to know – “will house prices continue rising?” To help answer this question, Tim Stafford, senior valuer and head of research at WBP Group, examines the critical factors that have got us to where we are today.

While speculating on the future of house prices is a national past time, I think Howard Marks (the founder of Oaktree Capital, who invested more than $10 billion during the Global Financial Crisis) makes an important point;

“We never know where we’re going, but we sure as hell ought to know where we are. I can’t tell you what’s going to happen tomorrow, but I should be able to assess the current environment.”

So, where are we?

The period between 2010 and 2017 saw solid and consistent growth in Australian house prices driven by a combination of above-average population growth, demand from international investors (especially Asia), a stable Australian economy and historically low interest rates. Eventually, the market peaked around the end of 2017.

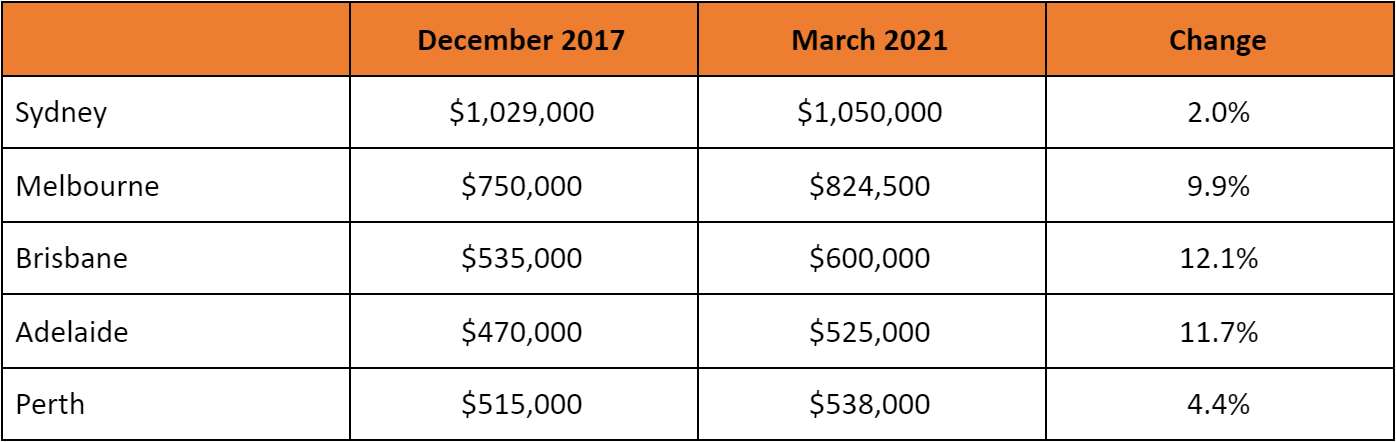

Change in median house price since last market peak

Source: Australian Bureau of Statistics

If you compare the change in median price from the last peak to the most recent figures from the Australian Bureau of Statistics (ABS), you see only modest growth, especially in Sydney. Why is that so?

House prices fell nationally through 2018. While Brisbane, Adelaide, and Perth experiencing only a minor drop, Melbourne and Sydney experienced significant falls, dropping 8.7% and 15.5%, respectively.

You couldn’t look at a newspaper in 2018 without seeing an article predicting doom and gloom for the property market. Many factors contributed to the pessimism, including poor affordability, the Banking Royal Commission, banks raising interest rates independent of the Reserve Bank, and a cut back in foreign demand due to changes in government policy.

It wasn’t until the first half of 2019 that the market eventually bottomed out.

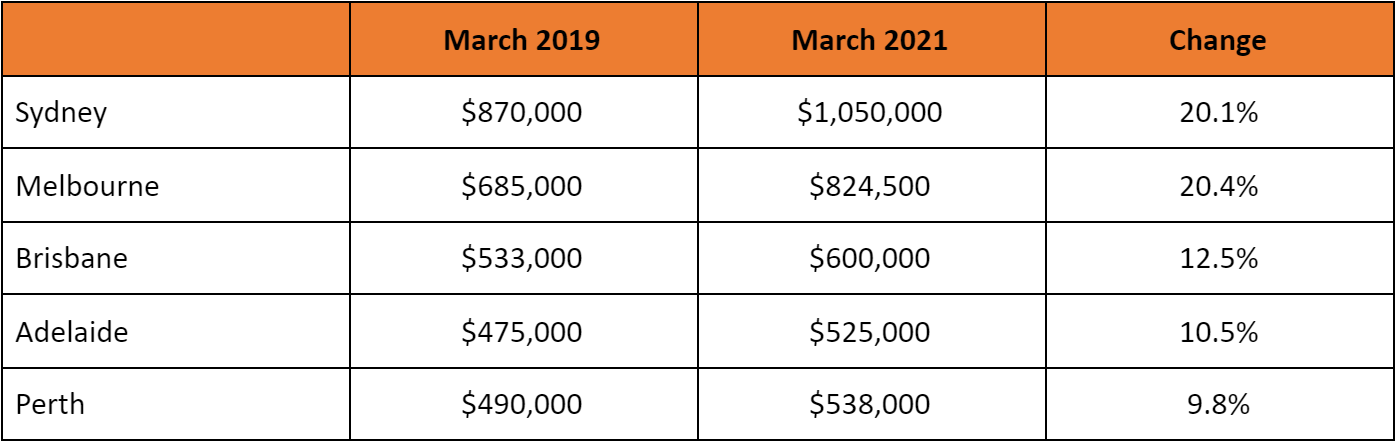

Change in median house price since the bottoming of the market

Source: Australian Bureau of Statistics

In Melbourne and Sydney, the change in the median house price from the bottom of the market has been dramatic, with much of this growth occurring in just the last twelve months. And as usual, it is these two markets that are driving house price growth nationally.

The most recent results from CoreLogic’s Monthly Housing & Economic Chart Pack, July 2021, showed:

- Australian dwelling values rose 13.5% in the 2020-21 financial year.

The highest annual growth rate since April 2004. - Australian dwelling values rose 6.1% in the June quarter.

Down from a recent peak of 7.0% in the three months to May 2021 – the highest quarterly growth rate since November 1988.

Throughout WBP Group’s five state offices, we have been astonished by some of the auction results we’ve seen over the last 12 months. In Elderslie, 60km west of Sydney’s CBD, a 10-year old four-bedroom home purchased in June 2020 for $660,000, resold in February 2021 for $755,00. A 14% increase in only seven months. And in Burleigh Waters, on Queensland’s Gold Coast, a renovated four-bedroom home purchased in November 2020 for $1,550,000, resold three months later for $1,675,000. An 8% increase.

WBP Group director Greville Pabst had this to say – “The growth in property values over the last 12 months, especially for established family homes, has been the strongest I have experienced in my 30 years in the property industry.”

Interest rates have played a critical role

It has been more than a decade since we last saw an increase in the official cash rate. On the 3rd November 2010, the Reserve Bank decided to increase the cash rate by 25 basis points to 4.75%. Since then, the RBA has lowered their rate 18 consecutive times to reach 0.1% today.

If you’d borrowed $500,000 in November 2010, your monthly repayments would’ve been approximately $3,500 based on an interest rate of 6.75% and a loan term of 25 years.

If you apply that same monthly repayment of $3,500 to today’s rate, you could now afford to borrow $815,000 based on an interest rate of 2.1% and the same loan term.

- Borrowing capacity has increased by more than 50% in the space of 10 years

Without substantial growth in wages, record-low interest rates have enabled homebuyers to significantly increase the amount of money they can borrow without raising their monthly repayments. This increase in borrowing capacity is one of the fundamental reasons we’ve seen house prices increase.

And as the cash rate reached a level unthinkable to many economists only two years ago, loan commitments have skyrocketed. It seems a significant number of Australians don’t want to miss this once in a lifetime opportunity. The most recent figures from the ABS showed;

- New loans for housing increased by 95%

In May 2021, new loan commitments totalled $32.6 billion – 95% higher than the same time last year and 89% above the long term average.The results of this surge in lending are now evident.

CoreLogic’s figures show that dwelling values for every Australian capital city except Perth and Darwin are at record highs.

Structural issues shaping the market

While interest rates are a big part of the story, structural issues are also noticeably impacting the Australian housing market. These issues have affected both supply and demand and have contributed substantially to the surge in house prices.

RBA governor Dr Phillip Lowe, in his July 2021 address to the Economic Society of Australia, outlined what he believes these structural issues are;

- Strong demand to live in fantastic global cities on the coast

- A desire to live on large blocks

- Chronic under-investment in transport

- Government incentives and taxation – first homeowner guarantee, HomeBuilder, negative gearing

Rates will rise – but when?

While house prices are surging, Dr Lowe made it quite clear in his July 2021 address, “the RBA will not raise interest rates to choke off house prices”. While an increase in the cash rate would cool the housing market, his view was that this would be a bad result for the overall economy.

Instead, Dr Lowe advised the RBA will focus on achieving its goal of full employment and an inflation rate consistent with its target range of 2-3%. And based on their analysis, the RBA doesn’t see this occurring until 2024.

If interest rates remain at these levels for at least another two years, will house prices continue to rise? This scenario appears to be a strong possibility, especially in the short term, given the failures of both state and federal governments to address structural issues in the market.

However, affordability is starting to bite, especially for first home buyers. And while still positive, CoreLogic’s 28-day rolling change in the Home Value index has been trending downwards since its peak in March, indicating that the growth rate is slowing.

So can the property juggernaut continue? Spring is just around the corner, and historically, it’s the busiest time in the real estate calendar. This will be a true test of the market.